By John Considine

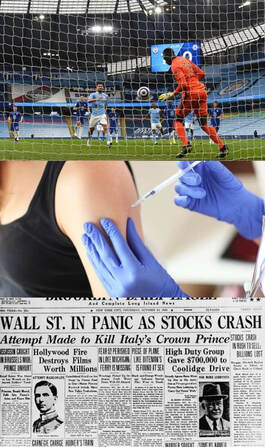

One of the most enjoyable workshops that I have attended was on the subject of coaching games. As an introduction to the topic of defending, the speaker played a short video (here). It was designed to show that patience plays a large part in the art of defending. Sometimes inaction can be better than action. At around the same time, the sport psychologist Michael Bar-Eli was making a similar point in the Journal of Economic Psychology. Bar-Eli's paper examines data on penalty kicks and he suggests that goalkeepers would save more penalties by diving less.

Bar-Eli documents the background to this research in his 2018 book called Boost! How the psychology of sports can enhance your performance in management and work. After getting a Professorship in Ben-Gurion University, the Dean introduced Bar-Eli to Ilana Ritov. Ritov's research examined "inaction bias" in vaccinations. Too few people were getting vaccinated. After reading her research, Bar-Eli considered if the opposite bias might explain the behaviour of goalkeepers in penalty kicks. In the case of goalkeepers, he suspected that the bias was towards action rather than inaction. Ilena Ritov joined Bar-Eli and the result was the Journal of Economic Psychology paper showing an action bias. Goalkeepers could learn from the lion in the video above.

Bar-Eli and his coauthors explained their findings by reference to a paper by Daniel Kahneman and Dale Miller dealing with norm theory. An economist might have noted the similarities with elements of Chapter 12 from The General Theory of Employment, Interest and Money. This is the chapter where John Maynard Keynes discusses animal spirits - "a spontaneous urge to action rather than inaction". A quote from the chapter can be used to capture the explanation offered by Bar-Eli and his colleagues - "Worldly wisdom teaches that it is better for reputation to fail conventionally". The norm is for keepers to dive. The reputation of a goalkeeper who does not dive might suffer.

I was not surprised to read that the Journal of Economic Psychology paper was "chosen by the New York Times Magazine as one of the significant highlights and most innovative research breakthroughs of 2008". I would recommend it because of the way the differences between the results and previous literature are clearly explained. Economists like Steven Levitt and Ignacio Palacios-Huerta had separately shown that penalty kickers and goalkeepers followed an optimal minimax strategy. Bar-Eli's paper is a model of clarity in explaining the apparent contradictions.

The year 2008 was at the start of the Great Recession. I smiled when I read a paragraph in the paper that explained the importance of understanding these biases for economics. It says that such an understanding is importance to investors and governments. Seventy years earlier, in his attempt to explain the Great Depression, Keynes did something similar in Chapter 12 from The General Theory of Employment, Interest and Money. At the start of the chapter he identified the need for data when he said "Our conclusions must depend upon the actual observation of markets and business psychology". He did not include observations of sports events. It was a period before big data and data analytics. However, his illustrative examples did consider the psychology of parlor games, such as card games and musical chairs. These were the games used by the mathematician John von Neumann to illustrate the minimax theorem he proved in 1928 - the same minimax theorem that economists like Levitt and Palacios-Huerta use on penalty kick in the 21st century.

It is not hard to imagine Keynes using the action bias in goalkeepers to explain the investor behaviour that contributed to the Great Depression. To take another quote from Chapter 12, he said these psychological "considerations should not lie beyond the purview of the economist".

Bar-Eli documents the background to this research in his 2018 book called Boost! How the psychology of sports can enhance your performance in management and work. After getting a Professorship in Ben-Gurion University, the Dean introduced Bar-Eli to Ilana Ritov. Ritov's research examined "inaction bias" in vaccinations. Too few people were getting vaccinated. After reading her research, Bar-Eli considered if the opposite bias might explain the behaviour of goalkeepers in penalty kicks. In the case of goalkeepers, he suspected that the bias was towards action rather than inaction. Ilena Ritov joined Bar-Eli and the result was the Journal of Economic Psychology paper showing an action bias. Goalkeepers could learn from the lion in the video above.

Bar-Eli and his coauthors explained their findings by reference to a paper by Daniel Kahneman and Dale Miller dealing with norm theory. An economist might have noted the similarities with elements of Chapter 12 from The General Theory of Employment, Interest and Money. This is the chapter where John Maynard Keynes discusses animal spirits - "a spontaneous urge to action rather than inaction". A quote from the chapter can be used to capture the explanation offered by Bar-Eli and his colleagues - "Worldly wisdom teaches that it is better for reputation to fail conventionally". The norm is for keepers to dive. The reputation of a goalkeeper who does not dive might suffer.

I was not surprised to read that the Journal of Economic Psychology paper was "chosen by the New York Times Magazine as one of the significant highlights and most innovative research breakthroughs of 2008". I would recommend it because of the way the differences between the results and previous literature are clearly explained. Economists like Steven Levitt and Ignacio Palacios-Huerta had separately shown that penalty kickers and goalkeepers followed an optimal minimax strategy. Bar-Eli's paper is a model of clarity in explaining the apparent contradictions.

The year 2008 was at the start of the Great Recession. I smiled when I read a paragraph in the paper that explained the importance of understanding these biases for economics. It says that such an understanding is importance to investors and governments. Seventy years earlier, in his attempt to explain the Great Depression, Keynes did something similar in Chapter 12 from The General Theory of Employment, Interest and Money. At the start of the chapter he identified the need for data when he said "Our conclusions must depend upon the actual observation of markets and business psychology". He did not include observations of sports events. It was a period before big data and data analytics. However, his illustrative examples did consider the psychology of parlor games, such as card games and musical chairs. These were the games used by the mathematician John von Neumann to illustrate the minimax theorem he proved in 1928 - the same minimax theorem that economists like Levitt and Palacios-Huerta use on penalty kick in the 21st century.

It is not hard to imagine Keynes using the action bias in goalkeepers to explain the investor behaviour that contributed to the Great Depression. To take another quote from Chapter 12, he said these psychological "considerations should not lie beyond the purview of the economist".

RSS Feed

RSS Feed